Incorporate Rates, Contributions, and Eligibility

After completing this unit, you’ll be able to:

- Explain the relationship between rates, contributions, and eligibility.

- Set up rate plans that align with carrier-negotiated premiums.

- Configure contribution plans to distribute costs between a client and its employees

- Define eligibility rules that determine when employees and their dependents qualify for coverage.

Aligning Rates, Contributions, and Eligibility

In the previous unit, you explored how Insurance Brokerage helps you model products, configure policies, and manage the policy lifecycle. But structuring policies is only half the equation—effective brokerage also depends on managing rates, contributions, and eligibility with precision. These elements answer key questions about the cost of coverage, who qualifies for it, and when, and who pays for it.

Brokers and clients work together to select carriers, negotiate rates, and establish contribution models that align with budget and workforce needs. Eligibility rules ensure the right employees and dependents have access to coverage. These rules have to adapt as circumstances change to account for new hires, promotions, life events, and more.

Here are some key concepts.

-

Rate: The carrier’s charge for coverage, typically structured by tiers (Eligible Employee (EE), EE + Spouse, and EE + Family.) Rates drive total premiums and broker commissions.

-

Contribution: The portion of the premium employees pay, sometimes subsidized by employers. Contributions can vary by tier or employee class.

-

Eligibility: The rules that determine coverage qualifications, often based on tenure, employment status, or job classification.

In this unit, you discover how Cumulus Brokerage configures vital plan components for Sally’s Aviation. The coverage has to be cost-effective, compliant, and suitable for shifting workforce needs.

The Rate Plan Model

A rate represents the amount that a carrier charges employers for insurance coverage. Rates are usually structured by tiers, such as:

- Eligible Employee (EE)

- EE + Spouse

- EE + Child(ren)

- EE + Family

Rate configuration is critical for calculating premiums and forecasting commissions. Rate structures fluctuate annually based on enrollment counts, carrier negotiations, and benefit structures.

To organize and manage these rates effectively, you use rate plans. A rate plan is a container for one or more rate structures tied to a specific policy. Every rate plan is associated with a single policy, ensuring there’s a single home where all rate data lives. You can optionally specify a coverage for a rate plan if you want different rate structures within the same policy. If you don’t specify a coverage, the rate plan applies to the policy as a whole.

With this approach, you can manage rates at the policy level for simplicity or by specific coverage for more granularity. Either way, the policy ultimately controls all rate plans, so you’re guaranteed consistency in how premiums are set and recalculated.

Rate plans fall into specific types that determine how calculations are applied across line items. This table introduces some common types.

Rate Plan Type |

Description |

|---|---|

Fully Insured Health |

Charges based on the rate and number of enrolled individuals per line item. |

Per Person Per Month (PPPM) |

Charges a fixed amount for each individual enrollee. |

Per Employee Per Month (PEPM) |

Charges a fixed amount for each enrolled employee, regardless of dependents. |

Flat Fee Based |

Charges a single fixed amount, regardless of employee or dependent count. |

Benefit Volume |

Charges based on the total value of coverages across all enrolled employees. |

Selecting the appropriate rate plan type helps ensure accurate and consistent calculations. Then calculations automatically adjust across all line items.

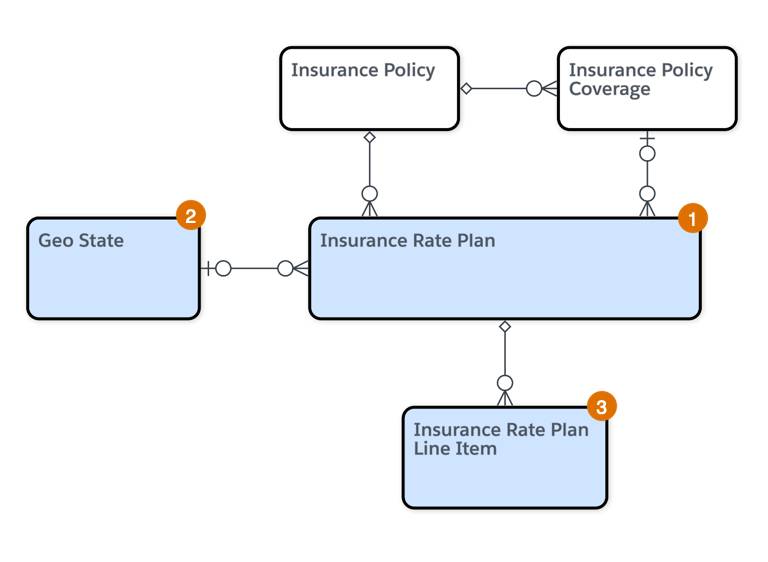

Here are the main objects for defining rate plans.

This table describes each object.

Object |

Description |

Scenario |

|---|---|---|

Insurance Rate Plan (1) |

Stores rate plan details such as premium amounts, billing frequency, and Rate Plan Type. Be sure to associate each Rate Plan with a policy. Optionally, you can also specify a coverage. If you leave coverage blank, the plan applies to the entire policy. |

For Sally’s HMO policy, different geographic locations require separate rate plans. |

Geo State (2) |

Represents a specific geographic area. |

Each of Sally’s rate plans connects to the appropriate Geo State—for instance, California and Florida. |

Insurance Rate Plan Line Item (3) |

Defines rates for each tier of the rate plan, including enrollment counts and calculated premiums. The number of tiers varies based on the plan’s design. |

Each of Sally’s rate plans includes three tiers: EE, EE + Spouse, EE + Spouse + Children. |

Next, explore how these components work together for speedy rate calculations.

Create a Rate Plan

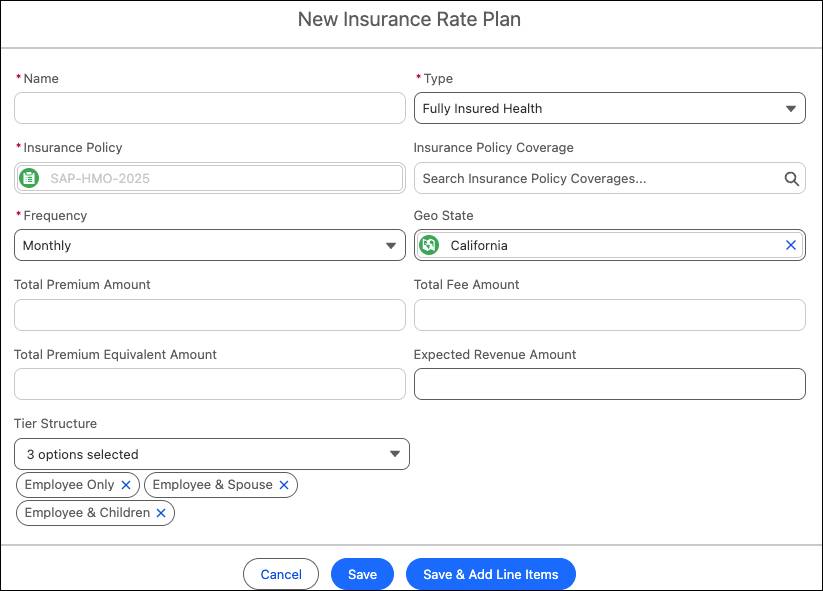

Rate structures can get complex with multiple tiers, coverage types, and premium frequencies, but Insurance Brokerage simplifies the process. Follow along as Julia configures the California rate plan for Sally’s HMO plan.

First, Julia creates a new plan from the policy record, specifying the type, payment frequency, and the tier structure.

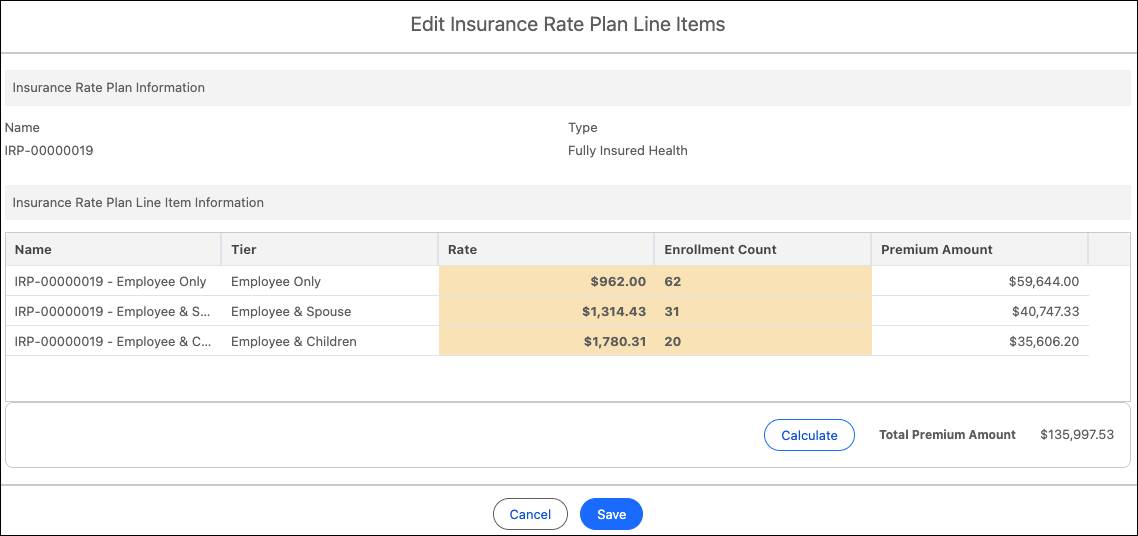

Next, she creates the line items, including the enrollment count and rate for each tier of the rate plan.

After entering the details, she clicks Calculate. And just like that, the premium for each tier and the total premium amount automatically display. Now Julia’s ready to create rate plans for the other geographic areas covered by the policy.

The Contribution Plan Model

Contributions determine how employers and employees share insurance costs. These plans vary by tier and by employee classification, aiming for a fair cost distribution.

Just like rate plans, each contribution plan is tied to a policy and you can associate a contribution plan with a specific coverage. If you don’t specify a coverage, the contribution plan applies to the entire policy.

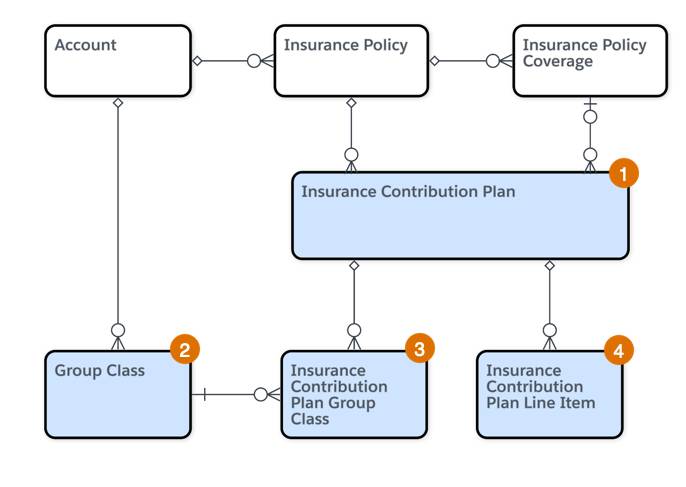

This table describes each object.

Object |

Description |

Scenario |

|---|---|---|

Insurance Contribution Plan (1) |

Stores plan details—such as contribution frequency, tax status, and contribution status—and always connects to a policy. Optionally, you can associate a specific coverage if the contribution applies only to that coverage. |

For Sally’s HMO Platinum policy, Cumulus creates separate contribution plans for different employee classes. |

Group Class (2) |

Represents an employee group classification, defined at the account level. |

Sally’s account has group classes for Executives, Management, Pilots Union, and Mechanics Union. |

Insurance Contribution Plan Group Class (3) |

Serves as a junction object linking a Group Class to a Contribution Plan. |

Cumulus assigns both union classes to a single contribution plan. |

Insurance Contribution Plan Line Item (4) |

Defines contribution amounts or percentages for each tier in a rate plan. |

Cumulus sets the monthly contribution amounts for each tier. |

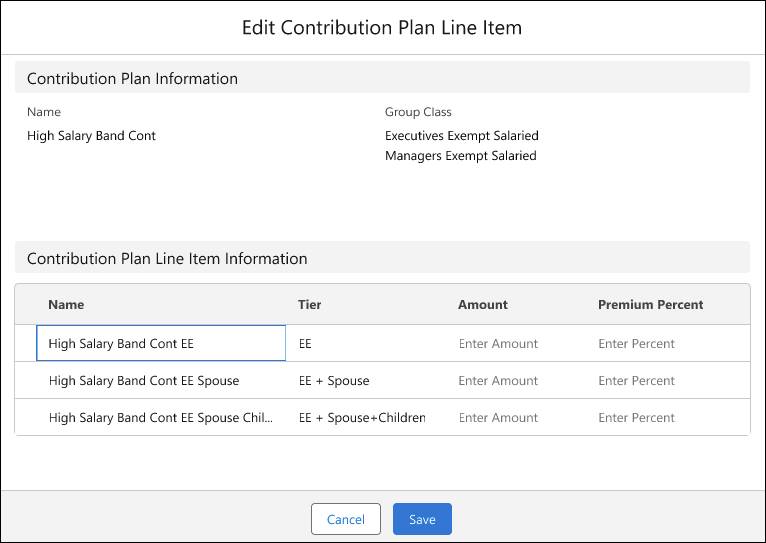

Create Contribution Plans

Follow along as Julia creates a contribution plan for Sally’s HMO plan for unionized employees.

First, Julia creates a new contribution plan record and adds the relevant group classes and tier structure.

Then, she defines line items with the contribution amounts for each tier.

For example, the High Salary Band Cont EE line item applies to eligible high-salary employees without dependents.

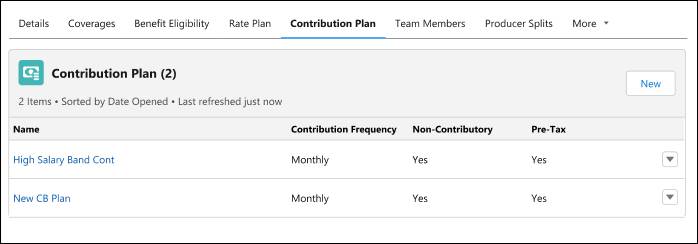

Once saved, the plan shows up on the Contribution Plan related list, and Julia repeats these steps for each additional contribution plan.

With rates and contributions set, the next step is defining eligibility rules.

The Eligibility Model

Eligibility rules define who qualifies for insurance coverage and when they’re eligible. These rules often correspond to employee status, tenure, or group class. By setting clear criteria up front, you ensure compliance and consistency across all your clients’ plans.

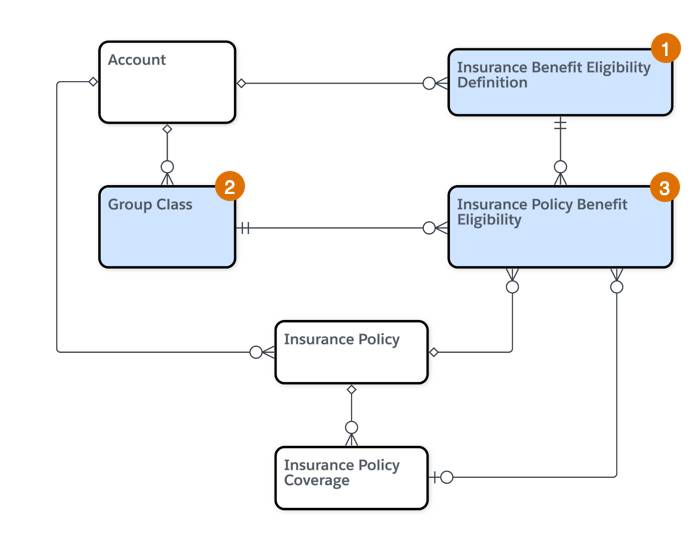

Here are the key objects involved in eligibility.

Here’s a quick summary of how these objects work together.

Object |

Description |

Scenario |

|---|---|---|

Insurance Benefit Eligibility Definition (1) |

Defines eligibility conditions at the account level, such as start/end dates and dependent eligibility. |

Sally’s eligibility rules include “coverage begins 30 days after hire.” |

Group Class (2) |

Represents a specific employee group, defined at the account level. |

Sally’s account has group classes for Executives, Management, Pilots Union, and Mechanics Union. |

Insurance Policy Benefit Eligibility (3) |

Maps a Group Class to an eligibility definition at the policy level. If needed, you can also specify a coverage for more granular control. If no coverage is chosen, the rules apply across the entire policy. |

Cumulus ties union classes to one eligibility definition and executives and management to another. |

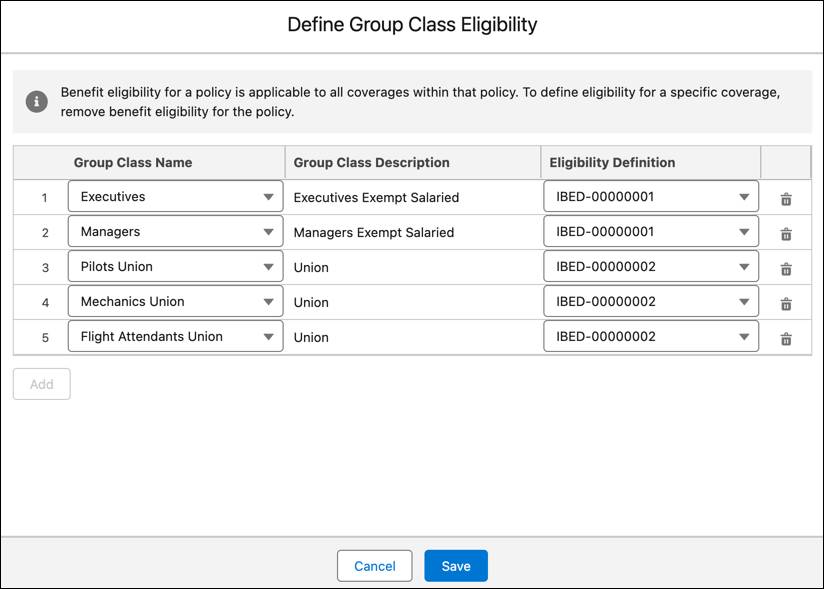

Define Eligibility for Plans

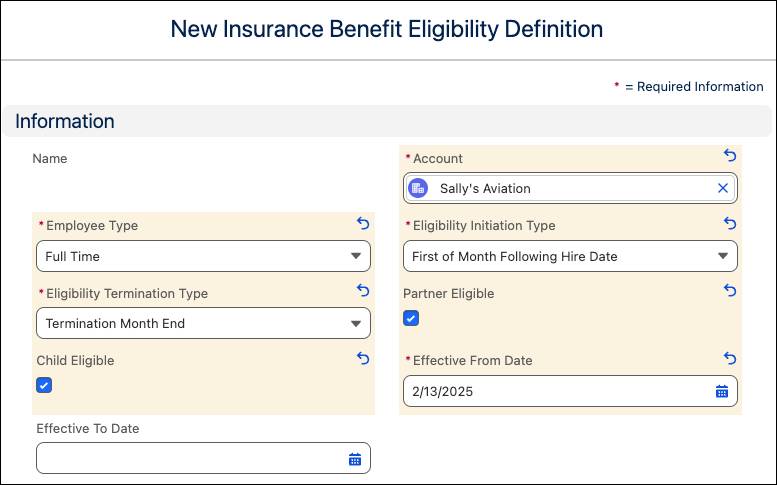

Follow along as Julia configures eligibility rules for Sally’s HMO policy and maps them to the appropriate classes.

First, she defines the eligibility definitions, specifying when coverage begins and ends, and who’s included.

This rule triggers eligibility on the first day of the month following the hire date and concludes at the end of the termination month.

Next, she assigns this eligibility definition to Sally’s Aviation HMO policy and maps each group class to the appropriate eligibility definition.

Because she maps the assignments at the plan level, these rules will apply to all coverages under the plan.

If any eligibility requirements shift later—say the waiting period changes to 60 days—Julia can simply edit the existing definitions, to keep the system accurate.

By configuring rates, contributions, and eligibility rules, Cumulus ensures each policy is financially sound and tailored to your client’s workforce and benefits strategies.

In the next unit, get ready to learn how Insurance Brokerage handles commissions and revenue calculations—giving you the full financial picture behind every policy.