Learn Blockchain Fundamentals

Learning Objectives

After completing this unit, you’ll be able to:

- Understand how traditional ledgers work.

- Identify what makes distributed ledgers different.

- Define blockchain and what makes it work.

What’s Up With Blockchain?

Maybe you’ve just heard about blockchain, but aren’t entirely sure what it is. Maybe you have a keen understanding, but are looking for more information on how you can benefit from it. Wherever you are in your journey, we’re here to help demystify the technology and offer some perspective on where it’s going and how you can benefit. Along the way, we’ll give some examples of how companies such as IBM are collaborating to advance the technology across industries.

It Starts with Ledgers

Doing business can involve a lot of people and organizations, especially in today’s connected world. Think about the journey simple coffee beans can make:

- The coffee beans are harvested by growers.

- Growers sell the coffee beans to brewers.

- Growers and brewers work with shippers to get the beans where they need to go.

- Brewers make delicious cups of coffee and sell them to customers.

Growers, shippers, brewers, customers. Let’s also add in banks and certifiers and coffee critics—it’s a lot to track. And that’s where ledgers come in, to keep track of these transactions.

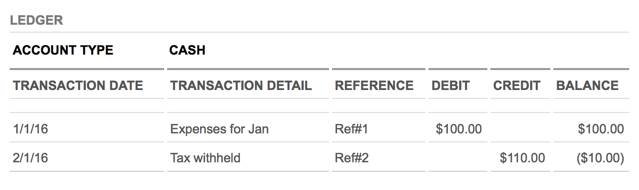

A typical ledger tracks specific information, such as the date of transaction, important details, and amounts transferred between participants (the growers, brewers, and shippers mentioned above).

So What’s the Problem?

Traditional ledgers can be inefficient, subject to error and tampering. Think about the coffee bean. Growers and brewers have their own ledgers. But when they do business with each other, they have to make sure the numbers add up.

When they don’t, it leads to disputes, from buyers requesting refunds and getting banks involved to people seeking legal action. Having to resolve disputes—and possibly reverse transactions or get additional insurance—can be costly.

To make things more difficult, having out-of-sync ledgers between participants leads to poor business decisions. At best, the ability to make a fully informed decision is delayed while these discrepancies are sorted out.

Moving Ledgers Forward

To improve the process, we’ve seen the introduction of distributed ledger technology. This is a type of database that is shared, replicated, and synchronized among participants.

No intermediary is needed. Every record in the distributed ledger has a timestamp and is encrypted, making it an auditable, permanent record of all transactions.

Blockchain is a Distributed Ledger with Super Powers

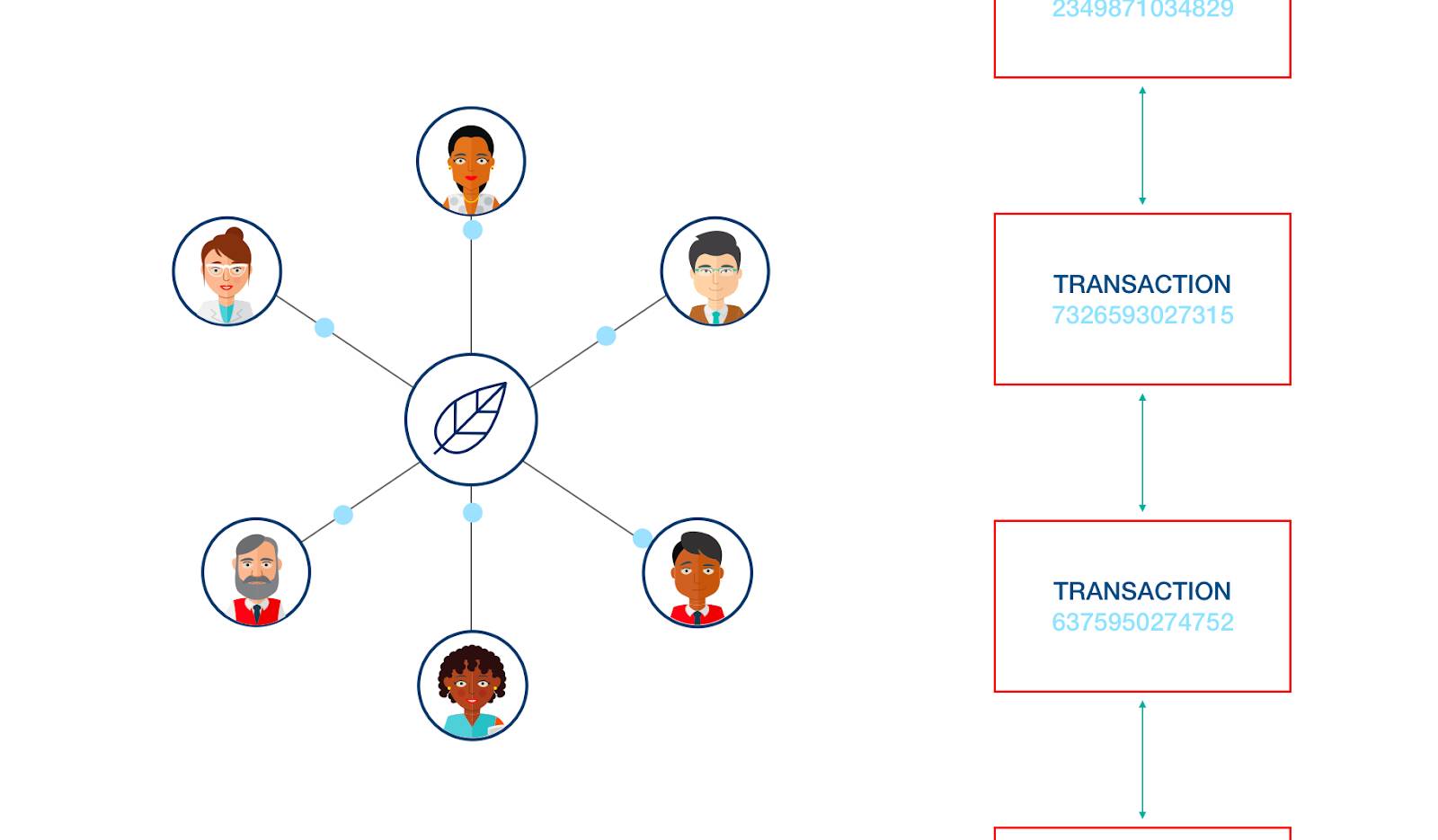

Blockchain is a type of distributed ledger that can record transactions in a public or private peer-to-peer network. But that’s not the innovative part. It takes things to the next level by how it works. With blockchain:

- Transactions are usually distributed across all members in the network. They're called nodes.

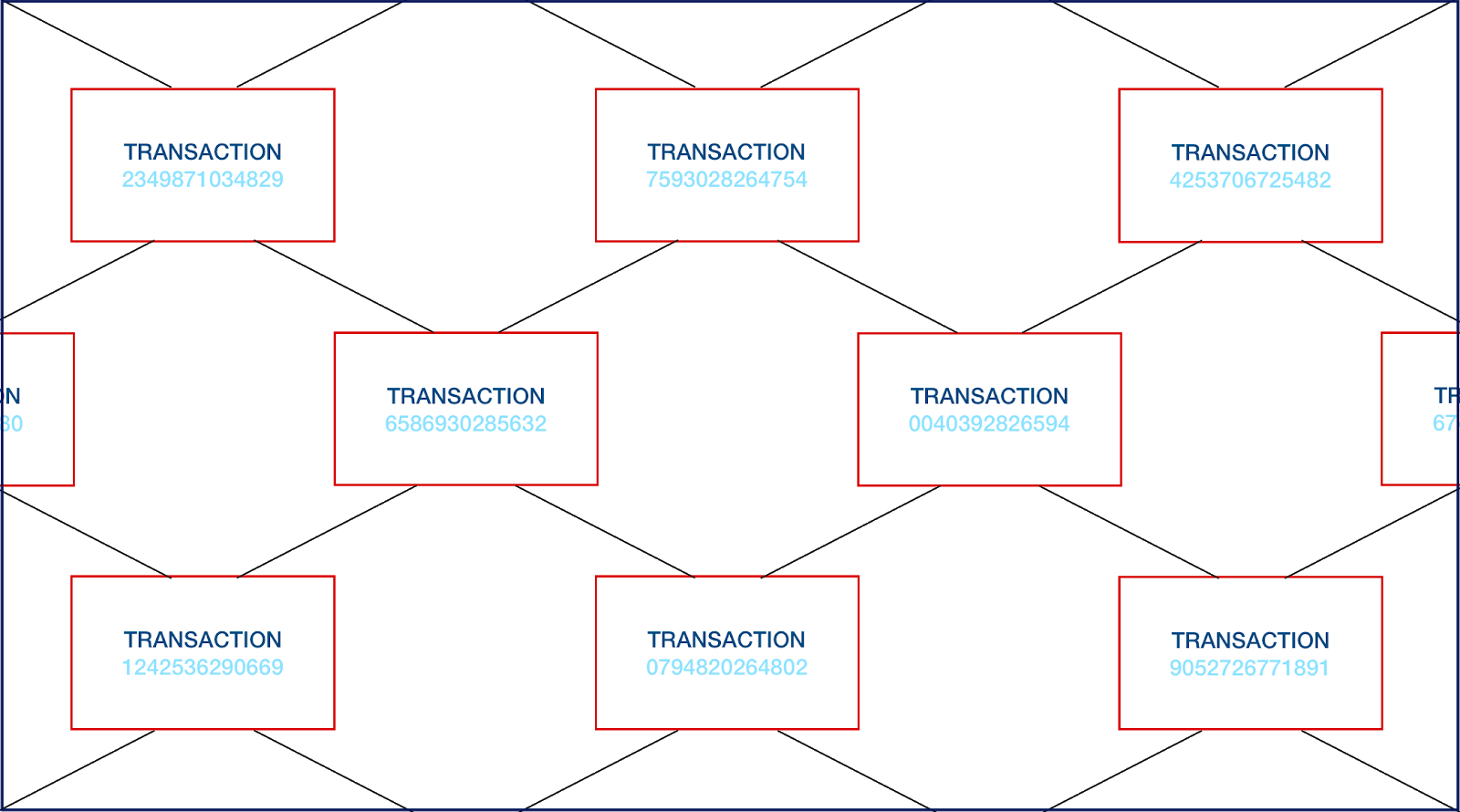

- Instead of one version, it tracks transactions in a chain of cryptographically signed records called blocks.

- All blocks are validated by the network. Then they are linked from the beginning to the most current—hence the name blockchain.

The blockchain acts as a single source of truth, as altering any existing transaction will break the chain.

That Was a Lot

You got all that, right? Okay, here’s a handy reference to come back to when explaining blockchain to your friends.

Key Term You Should Know |

Description |

|---|---|

Participant |

Any person or organization who is involved in conducting business. This can be the producer, supplier, partner, consumer/buyer, and so on. |

Transaction |

Actions, such when someone produces, sells, buys or trades, and takes ownership of an asset. |

Ledger/Business Ledger |

System of record where transactions are recorded. |

Distributed Ledger |

A database that tracks transaction data. It is replicated, synchronized among participants, and protected through encryption. |

Block |

A set of transactions bundled together to share with the network and lock into a chain to prevent changes. |

Node |

A participant in a blockchain network. |

Blockchain |

A distributed ledger technology that tracks transactions in a series of blocks instead of updating a single copy. It is designed to deliver more efficient transfer of goods and services and be a more reliable source of truth. |

Oh, but there’s more! Now that we know what blockchain is, let’s review how it can be used in your business and what value you can get out of it. See you after the quiz.