Understand the Technologies Behind Web3

Learning Objectives

After completing this unit, you’ll be able to:

- Describe main components of Web3.

- Define NFT, blockchain, and cryptocurrency.

The Building Blocks of Web3: Blockchain

In today’s digital-first world, someone can buy a tweet, develop digital land, pay without a traditional currency, and track down data to the 1s and 0s, all from the comfort of their personal device. The innovative technology that enables this transparency is the blockchain.

A blockchain is a system of recording information on a tamper-resistant digital ledger distributed across its entire network of computer systems. Each block on the chain contains transaction data that records each transaction on participants’ ledgers. The transactions are public and cannot be changed, tampered with, or erased once published.

The idea of a blockchain came to life as a solution for accurate and fixed time stamps, similar to that of a notary. This fundamental aspect is still present in technology today.

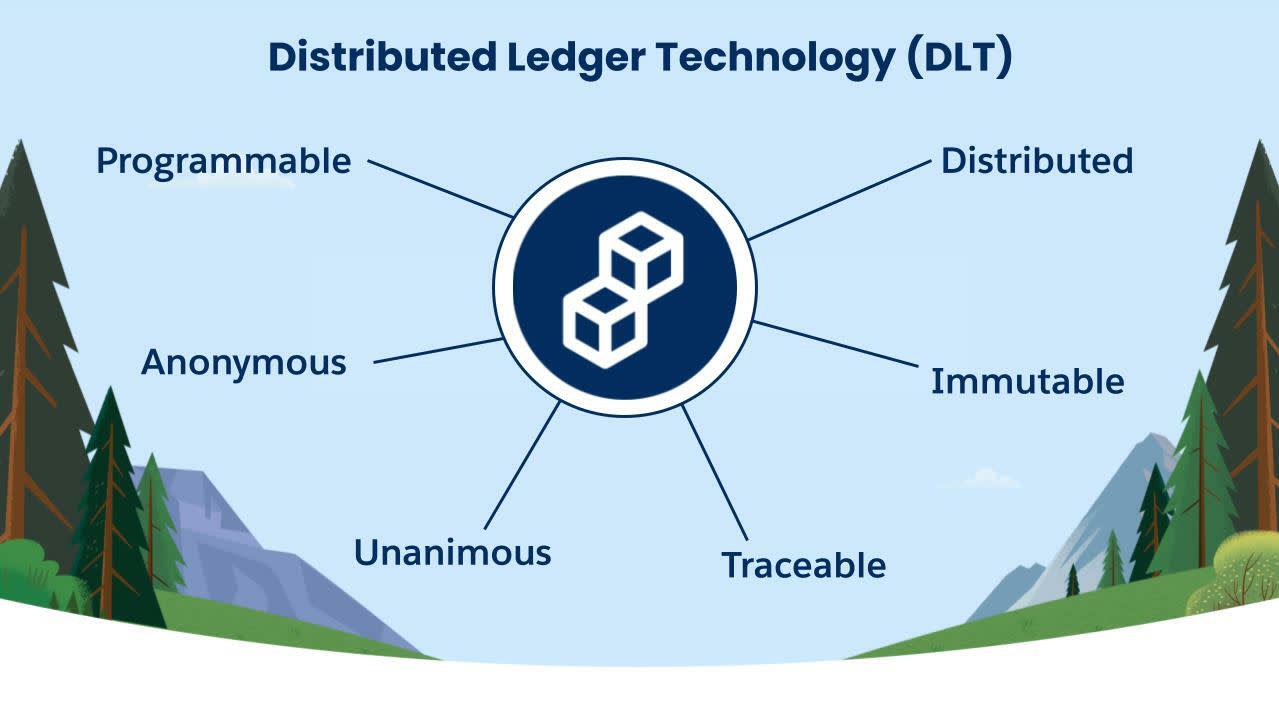

Blockchain is a type of distributed ledger technology (DLT), where these transactions are programmable, immutable, and anonymous.

Blockchains are constantly growing as blocks (transactions recording verified information) are added to the chain through every transaction. This increases the security of the entire ledger. The more blocks on the chain, the more secure the entire system becomes. This also allows regulators to easily identify if one of the blocks was tampered with, making hacking nearly impossible.

This is a young sector, and norms and standards are still emerging, including key issues such as sustainability. Companies, including Salesforce, have an opportunity to lead with values, and shape positive norms and benchmarks for using NFT and blockchain technology sustainably.

One key challenge in this space is related to sustainability. Many of the first generation cryptocurrencies (including Bitcoin) rely on proof-of-work (PoW) blockchains, which require the use of energy (that is, work) to perform transactions. This has resulted in significant energy consumption and carbon emissions, with Bitcoin consuming as much power per year as the country of Thailand (as of February 2022), according to the Digiconomist.

The industry is continuing to address sustainability issues as their technology evolves, as we’re seeing with new and upcoming proof-of-stake (PoS) blockchains. Based on current models, it’s believed that PoS blockchains drastically reduce the energy consumption seen by current-state PoW blockchains (by as much as 99.95% according to Olga Kharif’s Bye-Bye, Miners! How Ethereum’s Big Change Will Work, which appeared on Bloomberg.com in 2021). Additionally, e-waste from PoW blockchain use may be eliminated by switching to PoS, which does not rely on physical hardware for securing the network.

Companies and organizations exploring blockchain applications should put in place clear sustainability strategies to quantify, minimize, neutralize, and disclose environmental impacts resulting in net zero emissions while driving increased sustainability in the sector more broadly.

Now that we’ve discussed the power, purpose, and impact of Web3, let’s look at how this technology is utilized in cryptocurrencies.

What Makes a Currency a Cryptocurrency?

The simple answer is that a cryptocurrency is a nontraditional digital currency built on the blockchain. To expand on this, let’s look at how cryptocurrencies came to be.

On October 31, 2008, Satoshi Nakamoto sent a paper to a group of cryptographers familiar with blockchain technology outlining a new form of “electronic cash” called Bitcoin. In this paper he outlined how the distributed ledger technology (DLT) was combined with several other technologies and concepts to create the cryptocurrencies of today. These digital currencies are essentially electronic cash protected through cryptographic mechanisms instead of a central authority like a bank, company, or government.

Blockchain technology is the foundation of modern cryptocurrencies, most commonly referred to as crypto. They got their name because of the heavy usage of cryptographic functions paired with the decentralized ledgers.

This system allows someone to purchase, trade, and own a variety of things, including NFTs and real estate. And with more integration into our financial system, many more applications can be expected.

Next, let’s explore the role of NFTs in the Web3 ecosystem.

What Is an NFT?

An NFT (nonfungible token) is a digital asset that represents either digital or physical objects like art, music, event tickets, videos, and more. They’re backed by smart contracts, which allows them to have distinctive properties such as secondary sales and transferable value.

Here’s how NFTs work.

- NFTs exist on a blockchain, which is a distributed public ledger that records transactions.

- NFTs are blockchain agnostic, meaning they can be built on a variety of blockchains.

- An NFT is created, or “minted” from digital objects that can represent both tangible and intangible items.

- An NFT can have only one owner at a time, and an NFT’s unique data makes it easy to verify the creator and owner, and enables token transfer between owners.

- The creator writes a smart contract that defines the use and royalties of the NFT.

The Value of NFTs

So why buy an NFT, since anyone can copy an image or a video with an internet search and a few clicks? Well, buying an NFT gives proof of ownership of a unique digital asset, which can include virtual goods, in-game items, digital art, and more. Because they are built on the blockchain, the transaction and ownership history is public. This information is validated and records authenticity of the seller and the sole ownership. Just like with a physical asset, this can be collected, traded, or sold. In the case of digital art or when purchasing NFTs in secondary marketplaces, buyers should follow best practices to avoid potential scams and other risks. (More on this in a later unit.)

This technology enables trust and transparency between the buyer and seller by having full access to the historical transactions. The transparency provided by the public records can give the buyer insight into the seller's transaction history. As this technology develops, we’ll see companies creating products that will verify a seller or provide a risk rating based on past digital interactions.

Anyone can search online and find an image, video, or NFT for that matter, and download it to a device. But that’s just saving a copy of the file, not obtaining rights to the digital ownership of the file. For example, there are a lot of copies of Van Gogh’s Starry Night painting, but there’s only one original Starry Night. In theory, NFTs offer collectors the ability to own the digital rights to a piece of art, similar to owning the original Starry Night. (Note: This does not account for creators who copy and repost the original artist’s work as their own. These artists are infringing on copyright and can face serious penalties.)

Brand-new experiences are being built around rare digital and physical goods through the use of NFTs. Given that any digital thing can be an NFT, there are several possible use cases. Some companies have already capitalized on this idea, doing things such as launching an NFT system to verify the authenticity of sneakers, or creating NFTs from video clips of landmark sports moments so fans can own the best plays.

To demonstrate NFTs’ utility, here are a few more use cases. We may continue to see more as time and technology progress.

- Gaming asset: NFTs can be used as characters in video games and possess gamification capabilities. For example, games have allowed players to purchase NFTs that serve as their game avatars. And as players play, they can earn more NFTs, such as an ultra-rare shield to help them in battle or a new accessory to deck out their avatar.

- Key: NFTs can act as key to unlocking content, like a subscription to a sports or news magazine. Only the holders of the NFT are able to access the articles, updates, and statistics in the publication.

- Digital twin: NFTs can be purely digital; however, some projects have allowed the creation of digital twins. This can be something like offering virtual clothes that can be worn in the metaverse or sending an identical physical object to NFT owners.

- IP ownership: Projects can allow members to own the intellectual property of their NFT. The owner doesn't have to ask the NFT creator to use their avatar—they have the ability to create an entire business around the NFT.

- Governance/voting: NFTs can give owners voting rights on upcoming promotional merchandise and new platform/product releases, among other things.

NFTs can create authenticity, establish value, democratize access to global markets, and build community. Let’s take a deeper look at how NFTs use smart contracts and wallets.

Smart Contracts and Wallets

How does someone actually use cryptocurrency to buy an NFT? Let’s start by understanding how these transactions are tracked with smart contracts and how users employ wallets to buy and hold onto their NFTs.

First let’s go over a few NFT-related terms.

Smart contracts: These are simply computer programs (a few lines of code), stored on a blockchain, that run when predetermined conditions are met. They can be viewed as an application of Web3. They’re typically used to automate the execution of an agreement (or contract), so that all participants can be immediately certain of the outcome, without any intermediary involvement or time loss. They can also automate a workflow, triggering the next action, when certain conditions are met.

Wallets: A wallet is an app (or plugin), which enables users to access/retrieve, send, and receive digital assets. When a user acquires cryptocurrency, such as Bitcoin or Ethereum, they can store it in a wallet and from there use it to make transactions. There are two types of wallets.

- A custodial wallet is one created and secured by someone other than the true owner—for example, an account set up on Coinbase.

- A noncustodial wallet is one consumers create, own, and manage themselves. They often live directly within browsers (hot) or on offline devices (cold storage). Users self-manage security.

Smart contracts are used to protect buyers and sellers with automated contracts that are programmed to execute when certain conditions are met. These agreements can’t be changed or disputed once executed because smart contracts are immutable, distributed, and public.

With the ability to track when and to whom all NFTs are sold, smart contracts make purchasing NFTs at scale possible. This creates many possibilities, like enabling royalties for the original creator of an NFT, and offering protection for buyers.

To actually purchase an NFT, a buyer needs a wallet. There are many kinds of wallets, both custodial and noncustodial, each with pros and cons. Metamask, for example, is a noncustodial, browser-based wallet that’s currently the most popular to use with OpenSea, a popular NFT marketplace. With the rising popularity of NFTs and marketplaces, buyers should look into which wallet fits their needs best for security, ease of use, and compatibility with their marketplace of choice.

Wallets enable new capabilities for brands and users to interact. A few new possibilities include:

- New identity: Users may connect to a site and then provide access to any relevant information they want to share with the company for personalization. This provides a key to access the data, rather than sharing it.

- New experiences: In the near future, users may be able to have a wide range of assets in their wallets, essentially creating virtual versions of themselves. These 3D representations will allow them to try clothes on in real time and see the fit on their virtual selves.

- New ways to sign in: In the future, users may use NFTs on sites rather than passwords. Held in wallets, the NFTs will grant access without the need to remember passwords or have personal information stored in a brand’s network.

Now that you’ve learned about blockchain, crypto, and NFTs, let’s explore how all of these technologies can come together in the metaverse to create distinct digital experiences made possible through the engagement and participation of the evolving Web3 community.