See the Customer-Centric Sales Process in Action

Learning Objectives

After completing this unit, you’ll be able to:

- Outline a model for advancing and tracking an opportunity through specific stages.

- Explain how banks can use digital tools to ensure customer consent during the sales process.

- Describe how Salesforce helps banks measure employee performance against a holistic set of customer-focused metrics.

Metrics for Customer Retention, Engagement, and Consent

Dan’s manager, Kevin, is the head of sales for Cumulus retail and mortgage. He wants to review his team’s performance to make sure that the team’s sales practices align with the bank’s overall strategy of increasing customer retention and engagement.

Kevin’s key metrics aren’t simply the number of mortgages and accounts that his team sells. He is interested in the number of active customers who use their accounts regularly and continue to make their mortgage payments on time. So Kevin wants to verify a few things about Rachel’s history as a Cumulus customer:

- Rachel consented to opening her original checking account and continues to use it regularly.

- Rachel had a clear need for a mortgage before Dan sold her the product.

- Rachel secured her mortgage only after connecting with a Realtor, submitting an application, and reviewing necessary documentation.

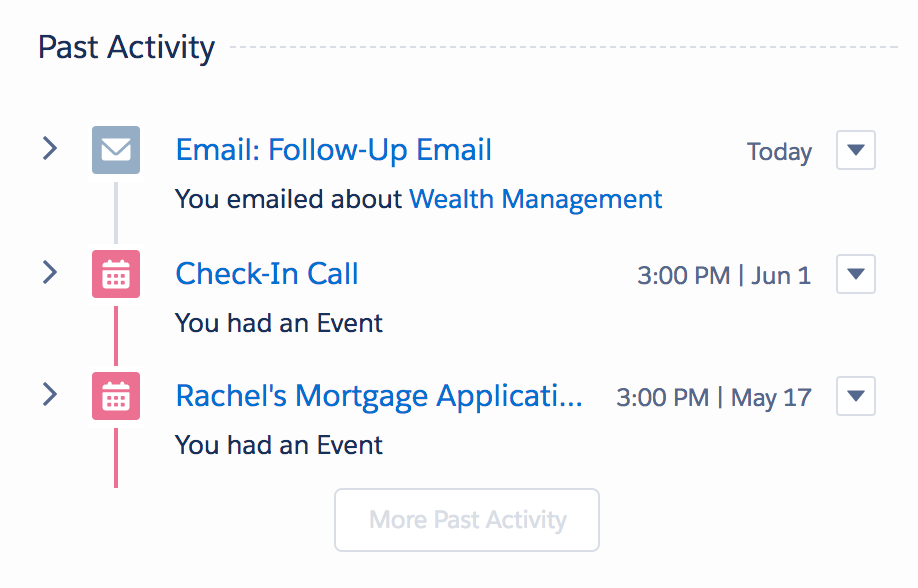

Because Salesforce contains a log of Dan’s communications with Rachel, as well as a record of her goals, Kevin can identify the specific customer needs that triggered each additional product that Rachel purchased. And thanks to opportunity management in Financial Services Cloud, Kevin can see the specific checkpoints that Rachel passed through during the process of purchasing each product. That helps Kevin verify that Dan followed the bank’s established procedures, which ensure that customers like Rachel understand the bank’s products and services and select the right ones to suit their needs.

For example, Kevin can see that Rachel consented to the opening of her checking account—the first product she purchased from Cumulus. Kevin traces the process from when Salesforce originally created her lead record, during her interaction with the Cumulus chatbot, to when she authorized the opening of her account after speaking with Matt, the Cumulus personal banker.

Salesforce automatically logged Rachel’s text message authorization for her checking account and stores this information alongside the e-signatures she provided on her mortgage, insurance policy, and wealth management documents. This information helps Kevin verify that Rachel consented to purchasing each of the Cumulus products and services that she uses.

A Clearly Visible Process from Start to Finish

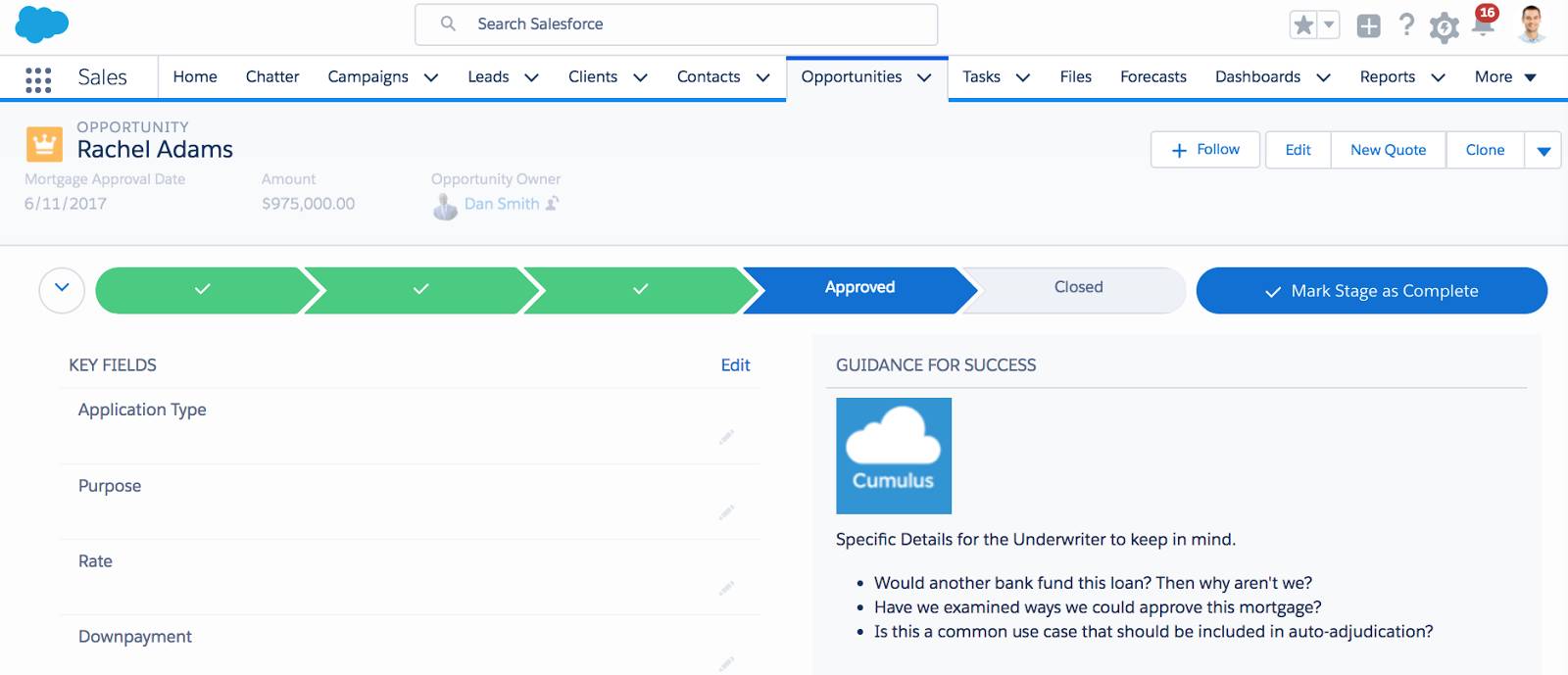

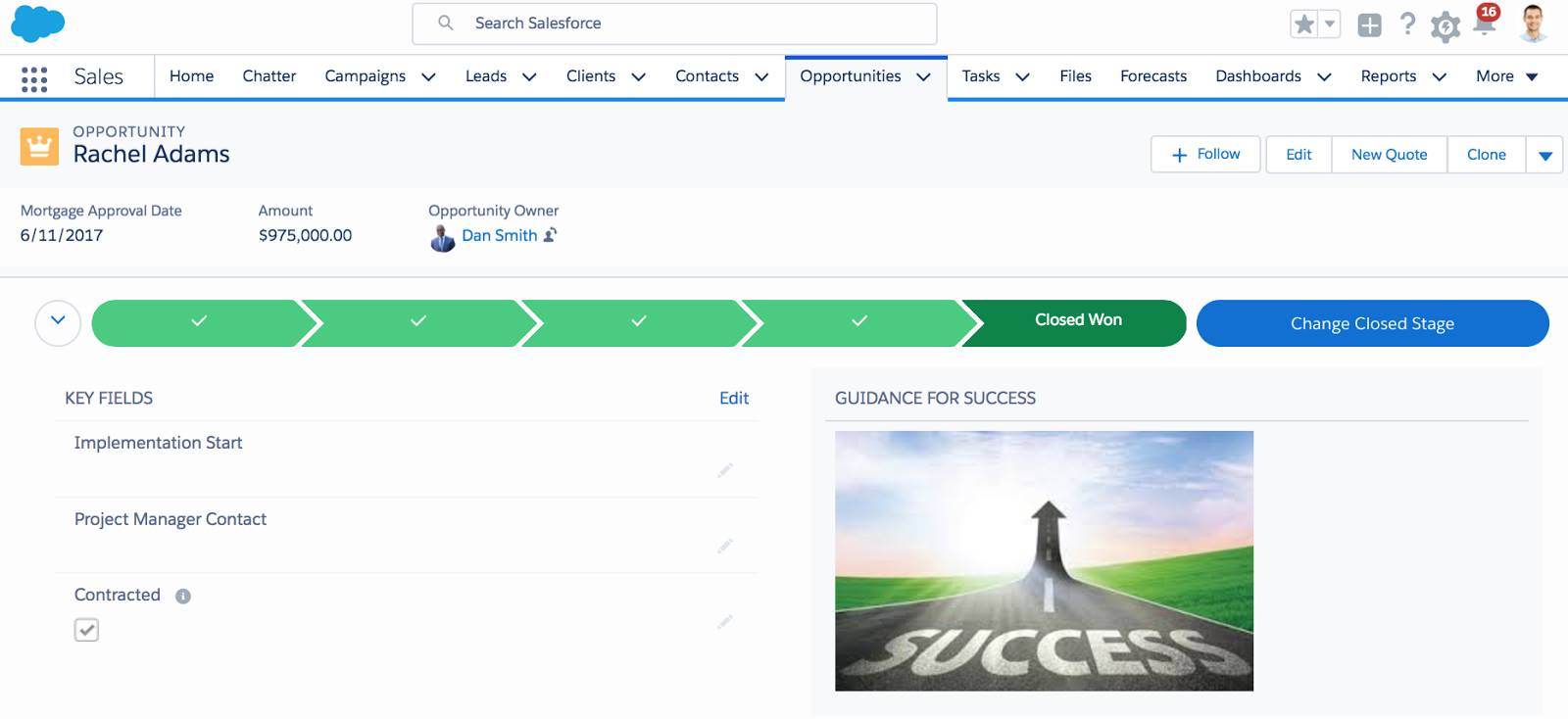

In addition, Kevin can see when Dan originally called Rachel and documented her goal of buying a home. Rachel’s move to New York City indicates a clear need for a mortgage, which explains why Dan offered to sell her that product. Kevin can then review how Dan moved Rachel through the required opportunity stages prior to her closing on a mortgage.

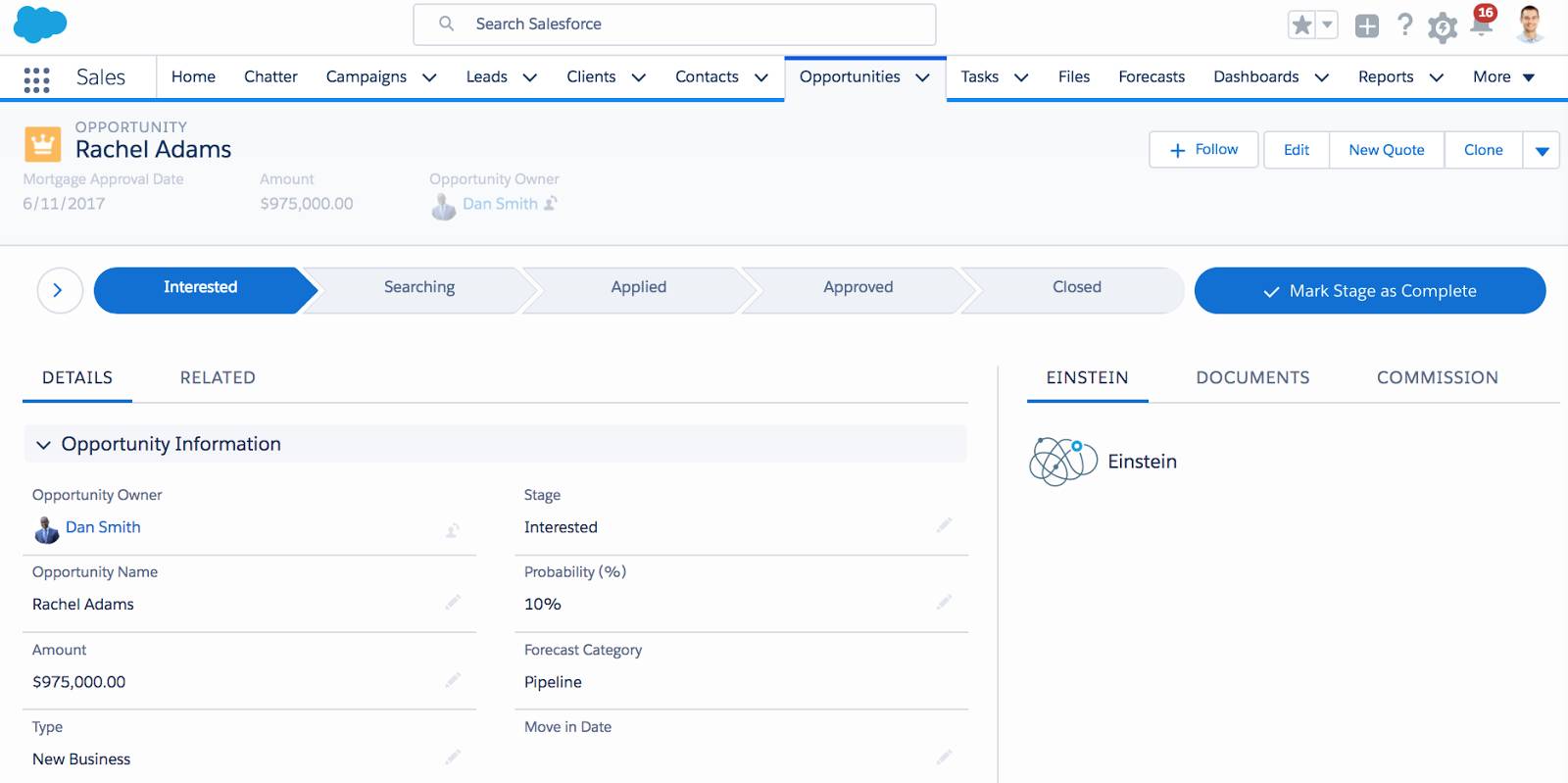

After the initial phone call, Dan created Rachel’s mortgage opportunity and left it in Stage 1, Interested.

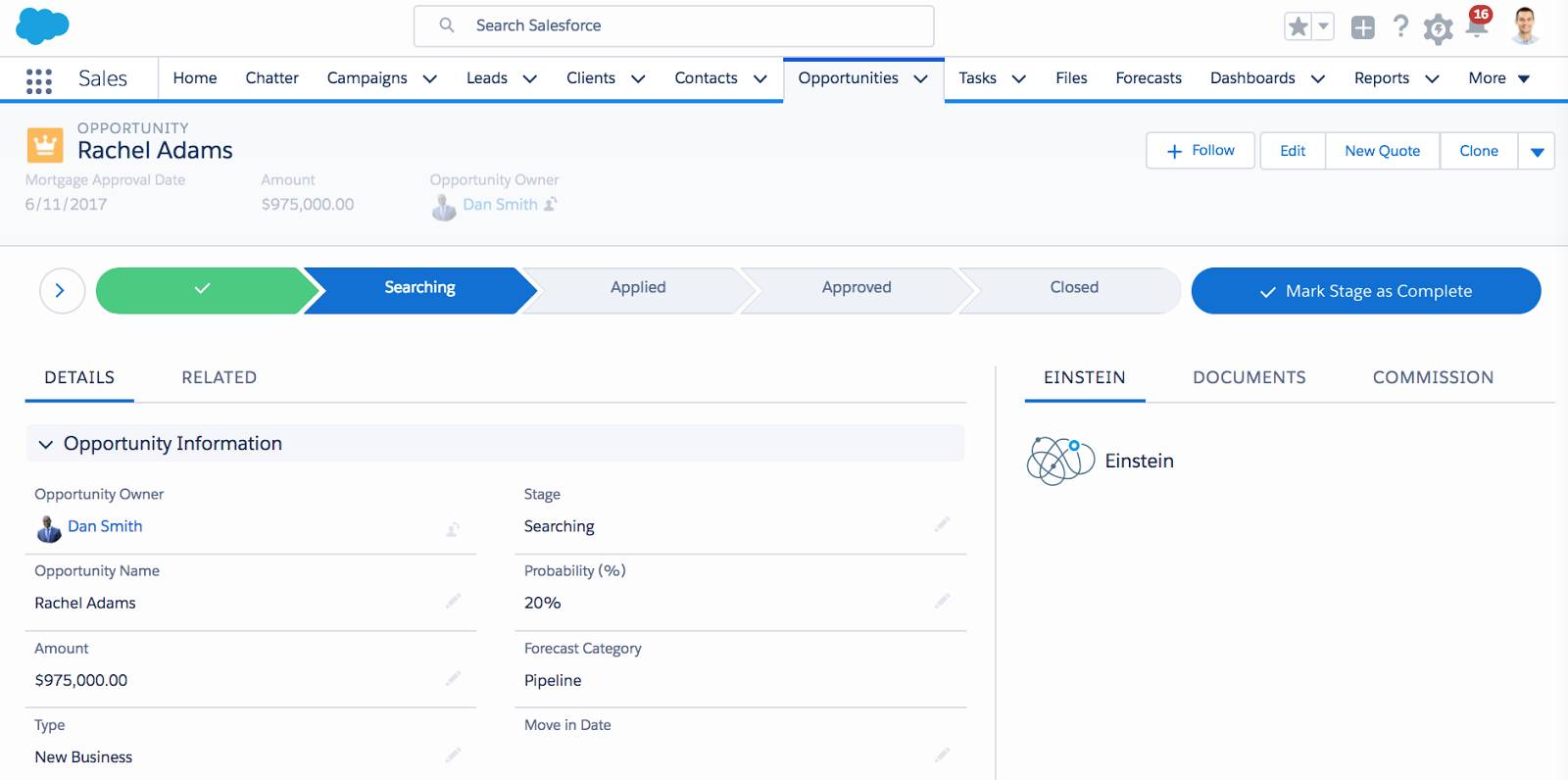

He moved her to Stage 2, Searching, after he followed up with Rachel and helped her find a Realtor to assist with her home search.

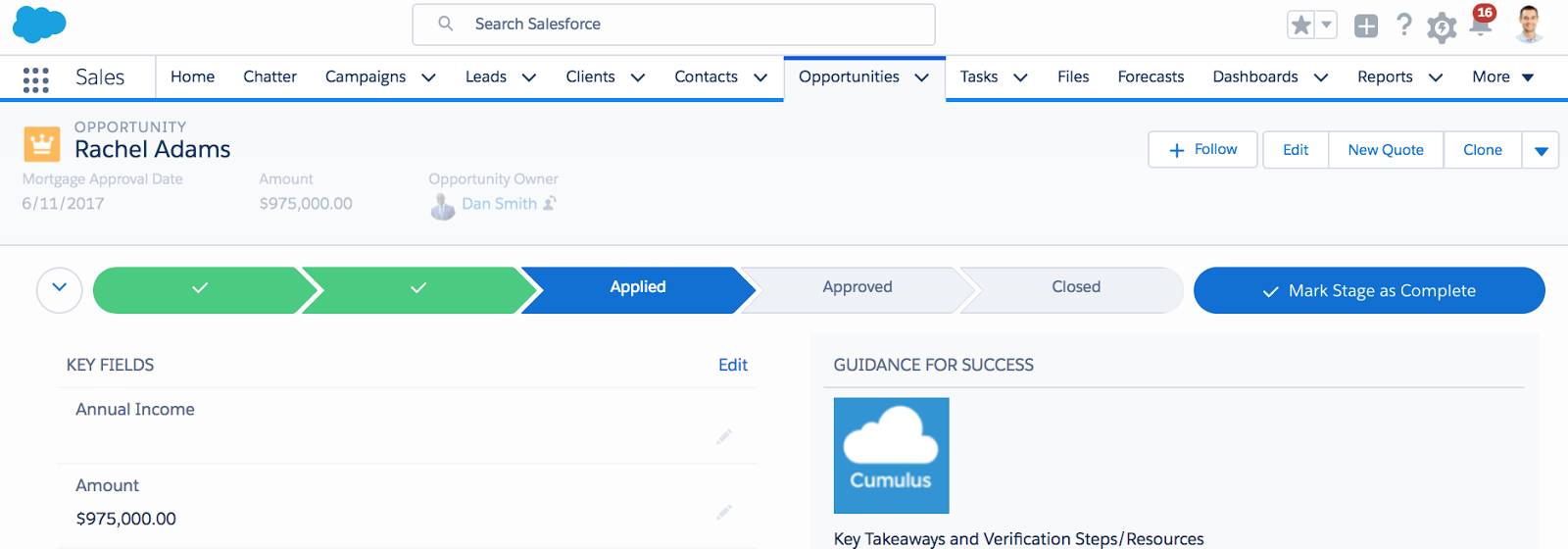

Salesforce automatically moved Rachel’s opportunity to Stage 3, Applied, after she applied for a mortgage through the Cumulus mobile app.

Salesforce automatically moved the opportunity to Stage 4, Approved, after Rachel received approval from the Cumulus mortgage team.

Finally, Dan was able to move the opportunity to Stage 5, Closed, only after Rachel submitted e-signatures that confirmed she had reviewed and agreed to the terms and conditions within her mortgage documentation.

After reviewing this sequence, Kevin is confident that Rachel was actively involved throughout the process and that the mortgage sale tied back to a real customer need.

Pinpointing a Job Well Done

Kevin also has a set of dashboards that show the Net Promoter Scores and account usage metrics that each customer records. He sees that Rachel is in the upper echelon of both metrics. Thanks to this information, Kevin can reward Dan for managing the relationship with Rachel so successfully for several years.

Even though the dashboards show that Dan’s volume of mortgage sales and cross-line-of-business referrals are lower than some of his peers’, his mortgage customers have a high NPS and typically convert into engaged users of other Cumulus products and services when Dan refers them.

Those high levels of customer satisfaction and account activity are directly in line with the bank’s goals of increasing customer retention and engagement, and Kevin has clear visibility into Dan’s contribution toward this success.

Throughout this story, Cumulus employees used Rachel’s needs to determine which products and services to offer to her. This kept Rachel happy and engaged as a customer, and it helped everyone on the Cumulus team reach their goals. With the right tools and processes in place, Cumulus aligned its incentives with Rachel’s financial interests and formed a deep and lasting relationship.