Open Claim Coverages

Learning Objectives

After completing this unit, you’ll be able to:

- Open claim coverages.

- Set reserves on claim coverages.

- Identify the records created when opening coverages and setting reserves.

- Describe how services create and update claim coverages.

Before You Start

Before you start this module, make sure you complete the following content. The work you do here builds on the concepts and work you do in that content.

Initiate Claims Management

In Claims Modeling for Insurance and Claims Creation for Insurance, you explored the elements and processes involved in creating a claim. These elements include the product model, power attributes, claim model, insurance policy, input JSON, and dedicated services.

Your claim is ready to go, and now it’s time to dive into how to manage it. This unit is your guide to opening a claim coverage, establishing reserves, and reviewing related records.

First, take a quick tour of how it all works. Then, peek under the hood at the services that make the magic happen. You’ll find this module especially helpful for designing or customizing a claims process.

Work with Claim Coverages and Reserves

Ernie Newton is a long-standing customer of Cumulus Insurance, a large, well-diversified provider of insurance services nationwide. Ernie owns a Cumulus homeowners policy, which contains several supplemental coverages, including a Personal Property coverage. This coverage protects against damage, destruction, and theft of his personal property. Recently, Ernie was the victim of the theft of some valuable furniture. To file a claim, he logs into Cumulus’s digital customer portal and submits a first notice of loss (FNOL).

After Ernie submits the initial claim details, the Digital Insurance Platform automatically creates a claim record and assigns a claims adjuster, Phil Sagad, to the new case.

After collecting more information about the claim, Phil gets straight to work managing the claim using his Claims Adjuster Workbench. First, he creates the claim coverages.

About Claim Coverages and Reserves

Claim coverage refers to the specific aspect of an insurance policy that applies to a given claim. When a policyholder files a claim, the insurer determines which coverage or coverages to open based on the nature of the incident and the policy's terms. Each coverage provides a defined level of financial protection against a particular type of loss, like damage to property or personal injury.

Each claim coverage has a critical component called a reserve. The reserve is an estimated sum set aside by the insurance company to cover potential future payments for a specific claim. The reserve includes costs for settling losses with the insured party and other related expenses like claim investigation, legal fees, and administrative costs. As the claim unfolds, the reserve adjusts to reflect the most accurate estimate for resolving the claim.

Open a Claim Coverage

Opening a claim coverage is straightforward. Navigate to the Financials tab on the claim record and select Open Coverage. Then, fill in the relevant details: the claimant, involved item, insured item, coverage, and loss reserve.

The screen shows an example of initial claim details.

The personal property coverage applies to the primary residence, and the estimated loss reserve is set to $85,000.00, based on the FNOL.

When you open the coverage, the Financial Summary chart automatically updates.

The chart displays an estimated financial exposure of $85,000 for the claim, which matches the loss reserve estimate. Because the claim has no loss or expense items, the chart doesn’t show any expenses, accepted losses, or pending losses.

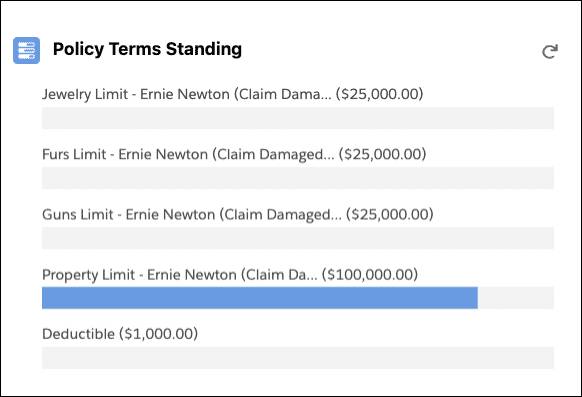

Here’s the Policy Terms Standing chart with the limits and deductible.

Notice the four total limits: one general property limit applies to the entire Claim Damaged Property coverage, while three sublimits target specific valuables within the coverage—jewelry, furs, and guns. A single deductible pertains to the entire claim, not just a specific coverage. Currently, only the Property Limit displays a pending amount because the loss reserve estimate covers the whole coverage, not individual sublimits. The deductible amount only changes when a specific loss item is created.

Review Claim Records

When troubleshooting potential issues on a claim record, always verify the configuration of the associated child records. Let’s check the records created after a claim coverage opens.

Navigate to the Related tab, and review the claim coverage record for the Personal Property coverage.

This record contains details about the claim coverage, including its loss reserve amount and the related claim and policy records.

Another new record, the Claim Coverage Reserve Adjustment, stores details about the loss reserve set on the claim coverage.

Any time you set or change the reserve amount, this record is automatically created, which links to the appropriate claim coverage.

Understand Claim Coverage Services

What happens behind the scenes whenever you open a claim coverage?

Essentially, the financials page calls a dedicated service named createUpdateCoverage that does all of the heavy lifting.

Based on the selections, the input data required for the service automatically populates with the necessary information.

Clicking Open initiates the service that opens the claim and generates the coverage.

Sometimes, you may get more information about a claim and need to adjust the estimated cost. In this case, find the loss item and modify the reserve amount.

After making the change, click Update to call the createUpdateCoverage service again. You can tweak the reserve amount here, but the other details of your claim coverage are locked in. If you want to make bigger changes, delete the original coverage and open a new one.

When you update the reserve amount, you automatically create a Claim Coverage Reserve Adjustment record for the claim coverage.

The new adjustment record captures the adjustment amount, which is $10,000.

Phil is impressed with just how easy it is to create, modify, and review claim coverages. He’s now ready to add more details about the claim.

In the next unit, learn how to generate loss and expense items for these claim coverages.

Resources